We very much value and respect your privacy. Please refer to Novo's Privacy Notice for additional details on information we collect as well as how we may use and share it.

You can call us at 1-866-862-7757, chat with us at www.novo.us (click the chat icon located at the bottom right corner), or email support@novo.us.

Policies are underwritten by KnightBrook Insurance Company, which is rated A- (Excellent) by A.M. Best.

No, we require the vehicles to be registered and insured in the same state.

All drivers insured by Novo are required to possess a license which matches the state listed in their policy usually within several weeks after purchase. The time period can vary by state, and you may contact us for that which is specific to your policy. Failure to adhere to our licensing requirements will leave your policy subject to cancellation.

If you move to another state where Novo is available, you will be able to maintain coverage with Novo. However, a change of address could impact your rate since location is one of the factors used to determine the price you pay. You can call us at 1-866-862-7757 to update your address. If it is located in another state where we do not offer coverage, we request that you cancel your policy with us once new coverage has been secured. If this does not occur, unfortunately we will be unable to renew your policy and coverage will expire at the end of the policy term.

We're working hard to expand to more states, but we don't have a set timeline for each one just yet. The best way to find out when we're available in your state is to check our website periodically. We’ll post updates there as we expand. You can also keep an eye on our social media channels for any major announcements.

Novo is currently available in the state of Arizona with plans to roll out across the country.

Novo offers personal auto insurance with 3 different pricing plans (see "What insurance plans does Novo offer?").

You get a quote and purchase a policy entirely online at quote.novo.us or contact us at 1-866-862-7757 and one of our amazing licensed agents will guide you. You can also write to support@novo.us and we will quickly get in touch with you.

Novo’s main location is in Lehi, UT and we have team members across the country. If you need to reach us by mail, please send to:

Novo Insurance

1881 W Traverse Pkway

Ste E #613

Lehi, UT 84043

Novo is open Monday-Friday from 8am-4pm MST. If you call outside these hours, please leave a voicemail or email support@novo.us and we will quickly get back to you.

Novo is redefining the car insurance experience — giving drivers back control of their rates with both stable and dynamic monthly pricing options. Because in a digital age where it’s possible to know exactly how everyone drives, it’s also possible to offer insurance to people who drive safely — with prices up to 40% less.

Because the safer you drive, the lower your rates should be. That’s why Novo offers a monthly pricing plan, so your premiums aren’t set in stone. It changes to reflect how you’re driving right now, showing you how to be an even better driver with real-time insights and coaching alerts. There is no device to add — the data will come straight from your car or mobile phone.

And that data is, and will remain, yours. Your privacy is of the utmost importance to us. That’s why drivers have trusted our parent company, Telenav, for 25 years with over 30 million vehicles on the road today using our connected services.

Disclaimer: Discounts offered and monthly rates are subject to change.

Novo keeps a percentage of the premiums we collect and pass along to our underwriting partner. This helps to pay for our expenses, invest in improving products for policyholders, and offer a delightful experience to all those who interact with us.

Novo offers competitive pricing for all our auto insurance plans. The greatest opportunity for savings comes from our dynamic premium option where your rate changes monthly based on your own driving behavior (see "What is the Flex plan?"). Instead of waiting 6 months to see your driving ability reflected in your price, you can start saving in a fraction of the time by maintaining safe habits while behind the wheel. Get a quote and sign up for a policy online at quote.novo.us or over the phone at 1-866-862-7757.

Insurance coverages are provided by KnightBrook Insurance Company, rated A- (Excellent) by A.M. Best.

Novo is a subsidiary of Telenav, one of the world's largest providers of connected car software and the leading navigation engine supplier to automotive manufacturers in North America. Innovating and changing the world is what has always driven us, and we've won J.D. Power awards for compelling consumer experiences for 5 years in a row. Our company has been at the forefront of delivering navigation and location-based services since our founding in 1999. We were the first to introduce them for mobile devices over 20 years ago and we've brought that same pioneering spirit to the insurance industry. Novo is structured as a managing general underwriter (MGU) which writes business on behalf of our partner underwriting company.

Your insurance ID card is the most important auto insurance document to keep in your car or wallet in most states. Not all states accept digital ID cards, so we recommend also keeping a printed copy as evidence that you are properly insured.

View them by logging in to your account, either on our website or through the Novo app.

View them by logging in to your account, either on our website or through the Novo app.

There are many reasons why your rate could go up or down at renewal, some of which may be reflective of the broader insurance environment while others could be unique to you. As described in one of our blogs, insurers are impacted by things such as price increases for used cars, repair parts, and skilled labor from inflation, supply chain issues, and worker shortages that increase how much they pay out in claims. We may also decide to decrease rates if we are able to pass along additional savings. If your situation has changed since your last renewal such as having been in an accident, received a speeding ticket or other moving violation, or gained/lost eligibility for a discount, those could also impact your rate.

If you choose not to renew your policy at the end of its term, you should call one of our customer service reps at 1-866-862-7757 or email support@novo.us before the renewal date. While we will be sad to see you go, it is important to get coverage with another carrier before your policy ends since driving without active auto insurance is illegal in nearly every state and could put you at serious financial risk in the event of an accident.

While it is infrequent and we don’t like to do it, Novo may decline to renew coverage for certain policies for a variety of reasons including DUIs, traffic violations, missed payments, and other reasons. Novo will provide notice at least 45 days in advance of your policy’s expiration if we deem a nonrenewal is necessary after a thorough review.

Your renewal will seamlessly take effect once the first payment is processed successfully. You will continue to be protected with no lapse in coverage as long as the payment is made on time.

These will be sent via email but both current and past renewal documents can also be accessed within the Novo mobile app.

Novo’s policies have a term of 6 months in length. Novo will send an email communication about your upcoming renewal at least 30 days in advance of your policy’s expiration and it will automatically renew in most states with no additional action necessary as long as you continue to make your premium payment. Your rate and other terms are subject to change, so it is important to look at the documents included or referenced in the renewal communication.

Novo does not charge any fees. However, there may be fees which we collect on behalf of a state such as Arizona’s Automobile Theft Authority fee of $0.50 for every 6-month policy term per vehicle and $25 filing fee for SR-22 forms. Any fees collected will be listed as part of the policy payment process.

You can log in to your account within the Novo app to see your past premium payments.

Once a cancellation is initiated, any payment owed by us is usually received within 3-5 days.

You will receive a refund for the portion of the payment that we did not provide coverage for, also called the unearned premium. For example, if you paid your bill for April, a 30-day month, in the amount of $100, and your cancellation took effect on the 16th, then you would be entitled to a refund of $50 since we provided coverage for the first half of the month but not the second half.

If your policy is still within the reinstatement period (which may vary by state), you must pay all premium due within our mobile app or by calling one of our customer service reps at 1-866-862-7757. In addition to paying all past due premium, you will be required to submit a statement of no loss which verifies that you were not involved in any incidents during the time that your policy was in canceled status. If your policy has been canceled for longer than the reinstatement period, then you will not be eligible for reinstatement and you will have to apply for a policy rewrite with a lapse in coverage.

A notice of cancellation (NOC) is a document that an insurer will mail to you (and your lienholder if applicable) if your payment is not received by the due date. The notice of cancellation warns of the date that your policy will cancel unless you make the required premium payment in time.

There is no late payment fee at this time, but we encourage you to pay by your premium due date to reduce the risk of policy cancellation.

Grace periods before cancellations can vary by state but will be a minimum of 7 days. We will send a reminder email if your payment is late, and you should pay the outstanding balance as quickly as possible to reduce the risk of a lapse in coverage or policy cancellation. You can contact us to find out what the specific grace period is for your state.

A missed or late payment can result in a lapse in coverage or the cancellation of your policy. We will send a late payment reminder email first, and you should make your payment as soon as possible after receiving it. Please call one of our customer service reps at 1-866-862-7757 in advance if you know that you’re going to have an issue with your next payment, and we will do our best to accommodate your situation.

A successful payment should be reflected immediately. If you refresh the page and do not see the payment reflected, you should reach out to a customer service rep for further investigation of the issue.

We will provide a confirmation email that the payment was successful or that there was an issue withdrawing funds from your payment method on file.

You can call one of our customer service reps at 1-866-862-7757 to process a transaction with a payment method that you do not want saved on file for future payments.

You can change it within the Novo mobile app or by calling one of our customer service reps at 1-866-862-7757.

No, you will be charged each month when your premium is due. Novo does not offer a pay-in-full option at this time.

If you need to change your due date to avoid failed payments, you can call one of our customer service reps to have it adjusted. You are unable to do this within our mobile app at this time.

Novo’s standard payment interval is once per month on your premium due date. We will process your first payment on the date you purchase the policy, even if your insurance will start at a later date. Then we will automatically process your second payment about one month after your policy start date, using the payment method on file. We will continue to automatically process a payment about a month apart until your policy is canceled. Due to the different number of days in each month, your billing statement can include between 28 and 31 days of base rate.

Yes, you can make a payment at any time within the mobile app once your invoice is available. Any changes to the policy after the payment is made that impact the premium amount (such as an endorsement) could result in an additional payment due.

A customer service rep can take a partial payment amount, but only if it is prior to the premium due date. If the request is on the premium due date or later, we are required to collect the full payment. If a partial payment is made prior to the premium due date, the remainder of the payment to meet the total due must be collected on or before the premium due date or the policy is subject to cancellation for nonpayment.

You may call one of our customer service reps if you’d like to split your premium with 2 different forms of payment. However, if one of the payments is declined and the premium due is not collected in full, your policy may be subject to cancellation. We’re working to add the ability to split payments in our mobile app.

Novo accepts all major debit and credit cards including Visa, Mastercard, American Express and Discover. Gift cards and prepaid cards cannot be used for any payments.

At this time, all policyholders are required to be enrolled in autopay.

Novo sets each policy to autopay by default. Your payment will be automatically scheduled and withdrawn on your due date.

Novo is paperless by default in Arizona.

You can pay online through the Novo app on your smartphone or by calling one of our customer service reps at 1-866-862-7757.

You will be notified of your upcoming premium payment at least 30 days in advance of the due date.

Novo is paperless and sends a billing notification via email each month. You can also log in to your account on our website or download the Novo app to see your next premium payment.

You are able to choose when your policy starts up to 14 days in advance. The soonest you can select a Novo policy to become effective is the day following the purchase date. Your first month’s premium is due at time of purchase with the next payment due 1 month after the chosen effective date.

If you're traveling within the United States (including U.S. territories Guam, U.S. Virgin Islands, and Puerto Rico) or Canada, coverage from your auto policy generally extends to a rental car just like you were driving your own vehicle, although some exclusions may apply. The same coverage listed in your policy would pertain (see "How can I access and view all my insurance documents?"). For areas outside the U.S. and Canada, your coverage may not apply or satisfy the local insurance requirements.

It is recommended that you purchase the optional collision damage waiver coverage from the rental company if you are renting a moving truck or similar vehicle. Your collision and comprehensive coverage may not transfer to a non-owned moving truck or van which is used for commercial purposes.

Many vehicle owners like to customize their vehicles with parts and accessories such as wheels, audio equipment, and exhaust systems. These enhancements are permanently installed in or on your vehicle by anyone other than the original manufacturer and could be items that alter either the appearance or performance of a vehicle. Anything installed by the dealer at the point of original sale usually wouldn't be considered custom and would be covered by comprehensive and collision coverages. Comprehensive and collision each provide up to $1,000 of coverage for custom parts and equipment. If you want more than $1,000 of protection in the event of damage or theft, you may add it while quoting and purchasing a policy.

An SR-22, also known as a certificate of financial responsibility, is a form to prove that you have auto insurance meeting the minimum coverages mandated by state law. It may be required for individuals convicted of certain driving offenses such as a DUI, driving without insurance, or multiple traffic violations. This form is filed by the policyholder’s insurance company directly with the state's department of motor vehicles (DMV) to demonstrate that the high-risk driver has adequate insurance coverage. If you are required to maintain this filing, you will be notified by the state. At this time, Novo is unfortunately not able to offer SR-22s or any other kind of financial responsibility filing for drivers in any state at time of purchase. However, if you are an existing Novo policyholder and it is determined that you require an SR-22, one of our customer service reps can assist with providing this form to you.

Roadside assistance is a set of services that can help when a problem with your vehicle occurs, leaving you disabled on the road. Most roadside assistance plans cover towing, battery jumpstarts, flat tire changes, fuel delivery, lockouts, and more. Typically, you'll pay an annual fee for this service, and it can be purchased when you buy your insurance from certain carriers offering it or from third-party roadside assistance providers. Unfortunately, Novo does not offer roadside assistance at this time, and you will have to purchase it standalone from another provider if you desire it.

Yes, we do offer $0 deductible glass as an optional coverage. Availability may vary by state.

Yes, Novo does not offer any coverage below the state minimum for the state you purchase coverage for. Minimum requirements may differ between states, and this may require you to adjust coverage amounts if you move to a new state and stay insured with Novo. Most states mandate that drivers carry a minimum amount of liability insurance and have the ability to provide proof of this insurance to register or renew a driver’s license.

States can have different required and optional coverages as mandated by law. “Full coverage” is an informal term which typically means that the policy has liability coverage plus comprehensive and collision. This would cover repairs or injuries for someone else but also for your own vehicle. It’s often required when financing or leasing a vehicle and provides additional peace of mind to the policyholder even if not required by any party. “Full coverage” does not mean having all available coverages like those such as loan-lease payoff and rental reimbursement which would need to be selected in addition.

Selecting the coverage that is right for you can be a difficult decision and everyone’s situation is unique. There is often a tradeoff between your budget for insurance premiums and your desired level of protection in the event of a claim. Most states require you to carry a minimum amount of liability insurance in order to register a vehicle or renew your license. Novo does not offer any coverage below the state minimum for the state you purchase coverage for so that you will be compliant. However, the minimum liability insurance required by the state may not be enough coverage to pay for damages after an accident. The person at fault could then be responsible for paying damages out of pocket, and no one can predict what amount that might be. A key question you should be asking yourself is whether you can afford to cover any damages exceeding your coverage limits without putting your assets at risk. Other considerations include the value of your vehicle and whether it is leased or financed since the company responsible may require additional protection for their interest. Once the vehicle is paid off, you would then be able to reduce your coverages and premiums. Regardless, we still recommend purchasing as much coverage as you can reasonably afford to best protect yourself from unexpected events on the road. You can call 1-866-862-7757 to speak to one of our licensed agents if you need help with your coverage selections.

A deductible is the amount of money that you pay out of pocket due to a covered loss before your insurance coverage pays. Deductibles are per incident so if you filed multiple claims in a year, you would have to pay your deductible each time. A lower deductible means that you’ll pay less out of pocket if an incident occurs, but you might have to pay slightly higher premiums. If you select a higher deductible, you’ll be able to save on your premiums but have to pay a larger amount when filing a claim. That's because you would pay a higher amount toward the repairs of your vehicle after a covered incident, and we would be responsible for the remaining balance. So, for example, if you had a $3,000 covered loss and your deductible was $500, you would pay $500, and we would pay the remaining $2,500. If your deductible was $1,000, you would pay $1,000, and we would pay the remaining $2,000. Choosing the right deductible depends on your budget and preference for saving on your premiums or reducing the potential out of pocket expenses if an accident happens. Please contact us if you need help with your deductible options.

A limit is the maximum amount listed in your policy that your insurance will cover in the event of a claim. If a claim exceeds the limit, the policyholder will likely be responsible for any remaining costs. When deciding on the limits for your policy, you can either choose to pay more per month for a higher limit (to provide yourself with additional protection) or you can pay less per month for a lower limit (but risk out-of-pocket expenses if the losses relating to an accident exceeds your limits). Policy liability limits are often written in a format that looks something like this: 100/300/100. The first amount of 100 is the per-person bodily injury liability limit of $100,000, while the second amount of 300 is the total per-accident bodily injury liability limit of $300,000, and the third amount of 100 is the per accident property damage liability limit of $100,000. Your limit amount options may vary by coverage type and state. Please contact us if you need help with deciding which ones are right for you.

We offer loan-lease payoff which is similar to guaranteed asset protection (GAP). It is an optional coverage for newer cars that pays for the difference between the amount you owe on your loan or lease and the value of your vehicle in the event that it is totaled or stolen. Since vehicles often start to depreciate in value as soon as they leave the lot, loan-lease payoff protects you if the loan balance is higher than the value of the vehicle. Without it, you would likely be personally responsible for any difference to the loan or leasing company. Comprehensive or collision coverage is required to be eligible for loan-lease payoff coverage, and it is limited to 25% of the actual cash value of the insured vehicle at the time of the loss.

Loan-lease payoff coverage will not apply to:

- Unpaid finance charges or interest

- Excess mileage charges or charges for wear and tear

- Charges for credit insurance or refunds due to the owner for credit insurance

- Past due payments and charges for past due payments

- The transfer or rollover of a previous loan or lease balance from another vehicle

- Collection or repossession expenses

While your options for insurance coverage may vary by state, the ones we currently or plan to offer in the future include:

Bodily Injury Liability — This covers the costs related to injuries to other drivers and their passengers in an accident you caused while you were driving. It pays for their medical care, loss of income, funeral costs, and additional expenses. Coverage can also pay for a legal defense if you're sued for causing those injuries. It is not intended to cover injuries to you as the policyholder.

Property Damage Liability — This coverage pays for property damage that you cause to other vehicles and/or property (like a building or fence) while you are driving. It can also pay for a legal defense if you’re sued for causing the accident.

Collision — This protects against damage to your vehicle caused by it hitting another vehicle or stationary object, such as a wall.

Comprehensive — This covers your vehicle for damage caused by something other than a collision such as hail, a branch falling on your car, or vandalism. It also would include repair or replacement of the windshield and other glass.

Medical Payments (MedPay) or Personal Injury Protection (PIP) — This pays for you and passengers in your vehicle who need medical treatment or have funeral costs after a collision regardless of who is at fault. It also protects you as a pedestrian if hit by a driver. PIP may include some additional benefits like coverage for lost wages and household services during the recovery process.

Rental — This will pay for a rental vehicle if yours is either inoperable or in the shop undergoing repairs after a covered loss such as a collision. It does not apply to mechanical breakdowns or your vehicle being unavailable due to servicing.

Uninsured Motorist (UM) and Underinsured Motorist (UIM) — These coverages pay for the medical expenses of you and any passengers after an accident when injuries are caused by another party who is either uninsured or doesn't have adequate insurance to cover the costs. They can also cover damage to your vehicle. Depending on the state, uninsured and underinsured motorist coverage may be separate, combined, or consist of up to 4 distinct coverages if each is split into bodily injury and physical damage. The main difference between UM/UIM and collision coverage is that UM/UIM only applies if an uninsured or underinsured driver was at fault and can cover medical expenses whereas collision can be used regardless of fault but only covers repairing or replacing your vehicle. UM/UIM would only cover medical expenses when an uninsured or underinsured driver was at fault while MedPay or PIP would apply regardless of fault.

Loan-Lease Payoff — This helps to pay off your auto loan or lease if your vehicle gets totaled or stolen and you owe more than its actual cash value. It will not cover the entire amount owed in all cases.

Coverages must be selected and premium paid to be applicable to your policy.

A change of address could impact your rate since location is one of the factors used to determine the price you pay. You can contact us to update your address. In-state moves should not be a problem, though out-of-state moves could be impacted by whether Novo offers coverage in that state.

Generally speaking, the insurance coverage follows the vehicle. If you were to have an accident while driving someone else's car, then the owner’s insurance would typically apply toward any damages first. In the event that the vehicle owner had no auto insurance or did not have enough auto insurance to pay the damages, then your policy may apply for the remaining damages. However, there are some exclusions when driving a vehicle not listed in your policy which you should refer to for additional details (see "How can I access and view all my insurance documents?").

Generally, you do not need to let your lienholder know that you’ve switched insurance companies unless you receive a communication from them. Novo will report your coverage once it begins, lapses, reinstates, renews, changes, or cancels on your behalf. This means that you at least need to let us know who the lienholder is.

In most states, proof of insurance will be required to legally drive your new car. If you already have an active policy, you can add it to your existing one. If you don't have a policy, you will need to purchase one. However, the soonest you can set a Novo policy to be effective is the following day, so you will have to purchase it at least 1 day in advance of driving the new vehicle.

Your Novo policy covers anyone listed in your policy as a primary driver and any additional drivers who have your permission to very occasionally operate your insured vehicle, including those outside your household. Any individuals who regularly drive your car should be listed in the policy. Failure to include these individuals could result in being ineligible for coverage for incidents while they were behind the wheel. Please refer to your policy for additional details on permissive use (see "How can I access and view all my insurance documents?") and reach out to us if you have any questions about whether an individual should be listed.

Only the primary named insured (PNI) and any applicable spouse of the PNI can make changes to the policy. If terminating coverage, the PNI must be the one making the request.

Policy changes can be made effective on the date requested, including the same day for some.

Any changes to your policy could increase or decrease your rate. This may include changes to coverages, deductibles, drivers, vehicles, and your address, among others.

To make changes to the lienholder listed in your policy, you can call us at 1-866-862-7757, chat with us at www.novo.us (click the chat icon located at the bottom right corner), or email support@novo.us.

To make changes to the vehicles listed in your policy, you can call us at 1-866-862-7757, chat with us at www.novo.us (click the chat icon located at the bottom right corner), or email us at support@novo.us.

To make changes to the drivers listed in your policy, you can call us at 1-866-862-7757, chat with us at www.novo.us (click the chat icon located at the bottom right corner), or email us at support@novo.us.

Yes, we do insure teenagers if they are legally able to drive with a valid driver’s license or learner’s permit. However, they must be on their parents’ policy if they are under the age of 18 since we are unable to offer coverage through their own policy.

No, they can be listed in your same policy as you, along with other members of your household.

The primary named insured (PNI), also known as the first named insured, is the first person listed on an insurance policy’s declarations page. While a policy may have multiple named insureds, the primary named insured is the policyholder and the one who is primarily responsible for the policy financially. The primary named insured is entitled to all of the policy’s coverage and receives certain rights and responsibilities that do not apply to others listed in the policy.

An excluded driver is a person who has been explicitly excluded from coverage in the policy. If this uncovered person is driving any covered vehicle, we will not be responsible for any damages or liability in the event of a collision. Some states have statutes and regulations that prohibit driver exclusions, and any individuals you may have desired to exclude must be considered for calculating the policy premium amount.

You, your spouse, and all resident relatives of driving age or older (according to your state), all regular drivers of the vehicles, and all children who live away from home who drive the vehicle, even occasionally, should be included in the policy. Additionally, all individuals who are titled owners of the vehicle other than those who are not household members, even if they do not operate the vehicle, should also be listed. Up to 2 drivers within your household may be excluded from your policy if you so choose, but they will not be covered in the event of an accident.

Your policy covers all listed drivers and vehicles, and up to 6 of each may be added. You are required to include all members of your household with a valid and active driver’s license or permit who will be driving the vehicle or they will not be covered in the event of an accident. If you let other individuals who are not part of your household borrow your car on a very occasional basis, they should be covered. This is called “permissive use.” Anyone with regular access to the vehicle must be listed. In the event of a claim, you will not be covered for household members who should have been listed in your policy but were not. Please refer to your policy for additional detail on permissive use and specific information regarding coverage. You can always reach out to us if you have any questions about whether an individual should be listed.

Yes, you are able to adjust your coverage, limit, and deductible selections in our quoting experience before purchasing a policy. These options will vary by state. If you need to make an adjustment after buying a policy, please contact us for assistance. Any changes may result in adjustments to your premium amount.

An endorsement, also called a rider, is a document that can be added to an insurance policy to make changes. They are used to include, exclude, or modify coverage to better meet your needs. Some examples include adding comprehensive and collision coverage, adding a child who just received his or her driver’s license, or removing a vehicle that you no longer own. After an endorsement is made, you will receive a new “amended declarations page” reflecting the requested changes.

While coverage will vary depending on your selections since some are optional, Novo’s auto policy can cover damage to your vehicle and also protect you financially if you damage someone else’s vehicle or property. Additionally, it can pay for medical bills if you, your passenger, or those in another vehicle were injured. Perils include accidents, vandalism, theft, weather, fire, and falling objects, among others. These may occur on the road or even while your car is parked. Carefully consider your coverage and limits when selecting them for your policy so that you get the protection you need, and contact us if you require assistance during the quoting process. In the event of an accident, you will only be protected up to the limits of your policy (see "How can I access and view all my insurance documents?"). Auto insurance is legally required in almost every state.

You can call us at 1-866-862-7757. Some changes can also be made within the Novo mobile app, and we are working to add more. We can help with changes to drivers, vehicles, coverages, limits, deductibles, lien/leaseholders, and personal information, among others.

You can call us at 1-866-862-7757. Some changes can also be made within the Novo mobile app, and we are working to add more. We can help with changes to drivers, vehicles, coverages, limits, deductibles, lien/leaseholders, and personal information, among others.

You can call us at 1-866-862-7757, chat with us at www.novo.us (click the chat icon located at the bottom right corner), or email support@novo.us. Some changes can also be made within the Novo mobile app, and we are working to add more. We can help with changes to drivers, vehicles, coverages, limits, deductibles, lien/leaseholders, and personal information, among others.

Most lienholders will accept a policy declarations page as sufficient for proof of coverage. The declarations page displays the type of coverage that you have on the policy along with the vehicles, drivers, and lienholder info.

A lienholder is any entity that holds a legal interest in the vehicle until its loan is fully paid off. This may be a financial institution such as a bank or credit union, the financing branch of the manufacturer (such as Stellantis Financial Services), or some other third party.

No, you will need to contact your previous insurer to cancel any active policy with them so that you are not double paying for coverage. You should reach out to them after buying a policy from Novo so that you don't have a gap in coverage.

Your cancellation can be made effective on the same day or scheduled for a later date of your choosing.

Novo policies can't be canceled online, but you may cancel it over the phone at 1-866-862-7757, via email at support@novo.us, or by mail to:

Novo Insurance

1881 W Traverse Pkway

Ste E #613

Lehi, UT 84043

Yes, you are able to switch insurers at any time, even if you just renewed your policy with another insurance company, although it could be subject to a small cancellation fee from them. When you cancel with another insurer, you should get a refund for the premium you paid in advance of your coverage period.

No, it won't affect your credit score. It is a "soft pull" which is a review of your credit file that is only visible to you and not lenders.

Certain types of claims or frequently filing them within a short period could impact your price at renewal. Claims history is one of the many factors used in calculating your rate. Data has shown that individuals with a history of making claims are at increased risk of doing so in the future, and additional premiums need to be collected to compensate for the elevated losses generally associated with that behavior. However, not every claim will impact the price at renewal.

While it may vary by state, Novo has at least 60 days to review your application and make any appropriate adjustments based on our underwriting review. This could result in a request for additional documentation from the policyholder and/or changes to the premium amount. There are numerous reasons why your premium could change such as not disclosing all accidents and violations, missing household members in your policy, or not meeting the criteria for a discount applied at purchase. When something like this happens, we will notify you. However, action may be required on your end to prevent adjustments to the premium amount or cancellation of your policy.

The soonest you can request a Novo policy to become effective is the day following the purchase date.

There are several factors which may cause your quoted premium to differ from the amount at purchase. It’s possible that self-reported information in the quoting process did not match third-party reports that we pull prior to sale, requiring an adjustment to the final premium amount. If some time has passed between the quote and purchase, our rates may also have been revised. Novo periodically files rate increases and decreases as well as makes improvements to our pricing model on a state-by-state basis that could influence your price, even if nothing else has changed for your situation.

Your quoted premium should be accurate at the time of the quote (if all requested information was accurately entered). While it is unlikely that your rate will change within a few days, we do periodically file rate increases and decreases as well as make improvements to our pricing model on a state-by-state basis. You can always purchase your policy now but set the effective date in the future to lock in your premium amount for the first term.

No, you can have up to 6 drivers and 4 vehicles on a given policy. Up to 2 drivers from your household may be excluded in the policy.

You can call 1-866-862-7757 to speak to one of our licensed agents.

Novo offers 3 different auto insurance plans, including several usage-based insurance options, so you can choose the one that best fits your needs: Classic, Next, and Flex (see "What is usage-based insurance?"). All provide the same coverage and limit options — the main difference is how your premium is calculated and adjusted over time. The table below provides a comparison of the key differences between the plans.

Only you, Novo, Novo's underwriter partners, and the vehicle’s manufacturer should have access to any data that could be potentially connected directly to you.

Anyone listed in the policy can view the Safety Score(s) once logged in to our mobile app.

Let us know right away if you sell a vehicle that is associated with your policy. Once it is removed, the next driver's behaviors will not impact your Safety Score and pricing. If you do choose to sell your car to a private party, feel free to recommend Novo — we always appreciate referrals!

Your Safety Score is vehicle specific. So, if you have more than one car on your policy, each will have its own Safety Score. For select Novo plans, this impacts the premium amount associated with that vehicle. Then, both are added together to calculate the total premium amount as shown in your bill.

If you already established a Safety Score, we would continue to use your most recent score to determine your rate. If you haven't yet established a Safety Score, we would use a default score for insufficient data collected.

For policies which require a mobile phone for data collection, a given trip may not be incorporated into your Safety Score if connectivity is lost at any point during that trip. For policies where we are obtaining driving data directly from a connected vehicle, the data will still be collected but delayed until connectivity is restored.

While the Safety Score is an input for some Novo plans, there are many other factors for determining the price of your policy (see “How do you calculate the cost of a Novo policy?”). However, without making any other changes such as adding/removing drivers or vehicles, the Safety Score is the only item that can cause your monthly premium to go either up or down within a given policy term for those on the Flex plan. The Safety Score does not impact monthly premiums within a term for any other plan.

Unfortunately, it is not possible to determine how much your premium will go either up or down simply by looking at the score. If your driving score improves by 10 points, for example, this could result in a different premium discount when moving from 60 to 70 versus 80 to 90. However, you may utilize the rate simulator within the Novo mobile app to estimate how much your premium will change if your Safety Score moves either up or down. Not all Novo plans utilize your Safety Score for pricing (see "What insurance plans does Novo offer?").

We update the score as frequently as we receive data from your vehicle or mobile phone. This can vary by vehicle but is usually at least daily.

While your Safety Score is continually updated based on new trips, how often it resets for billing is dependent on which Novo plan you are enrolled in. For those with the Flex plan, it will reset at the end of each monthly billing cycle but for the Classic and Next plans, it will reset approximately 1 month prior to the end of your 6-month policy term. Unlike the other plans, your Safety Score for those enrolled in Classic is for educational purposes and does not impact your rate beyond the potential 10% discount for sharing driving data. The exact dates of data collection for each billing cycle can be found within our mobile app.

Since data is tied to the vehicle listed in your policy, you can be sure that only trips taken by that vehicle are incorporated into the Safety Score. Programs from other insurance companies which collect driving data only from mobile phones are susceptible to errors (such as classifying a trip with you as the driver when you were actually the passenger in someone else’s car). Novo’s Safety Score may incorporate trips taken by all drivers regardless of whether they are listed in your policy. It is important to keep this in mind before agreeing to let anyone drive your vehicle.

You can reduce the driving habits that negatively impact your Safety Score including hard braking, rapid acceleration, and speeding. We also offer in-app coaching tips to help you improve your score and save even more money.

For the first month, your Safety Score will not display in the mobile app until you have completed a minimum of 5 trips with 200 miles in total. The Safety Score will reset near the end of each policy term for those on the Next plan. For those on the Flex plan, it will reset at the end of each monthly billing cycle. After resetting, you you will need to complete a minimum of 5 trips with 100 miles in total to see the Safety Score display again.

Novo collects a variety of information that can vary by vehicle make, model, and year. It may include latitude, longitude, timestamp, trip start/end location, and odometer. You may view our Telematics Privacy Notice for additional details. All data that is potentially captured from your vehicle can be found within the telematics consent agreement of the manufacturer.

We consider 3 factors per mile driven for our Safety Score: hard braking, rapid acceleration, and high speed. Hard braking is defined as decelerating at more than 8 mph per second. Rapid acceleration occurs when accelerating over 7 mph per second. High speed is declared when traveling at a rate above 80 mph. Novo encourages you to obey all traffic laws.

Novo’s Safety Score measures your driving performance based on how safely you drive. Risky events—like hard braking or speeding—can lower your score, while trips without these help to improve it. Your score is based on the number of risky events per mile driven. For select Novo plans, your Safety Score helps determine how much you pay for insurance.

All of Novo's plans are currently available in the state of Arizona and will be soon rolling out across the country.

The ADEPT Driver training program is an online technology-based accident prevention course. Novo partners with ADEPT Driver to promote safe driving. Drivers who complete an ADEPT Driver training course may qualify for a discount of up to 10% off their rate. When you or any driver on your policy completes an ADEPT Driver training course, just send us an email with your certificate of completion and we’ll apply the discount. The exact savings may vary.

Novo offers a variety of competitive discounts including Advance Shop Days, Distant Student, Good Student, Teen Driver, Driver Training, Homeowner/Mobile Homeowner, Multi Car, 3-Year Safe Driving, New Business 5-Year Accident Free/5-Year Claim Free, Continuous Insurance, New Business Novo Safety Program (NSP) Participation (first term only), Driving Insights (Classic plan only), and All-Star (Next plan only).

Novo’s personal auto policy isn't designed for commercial or business use. Therefore, any accident or damage resulting from a loss while the vehicle was being used for this purpose could result in a denial of your claim. Commuting to and from work would not count, but using your vehicle to perform activities such as delivering goods or driving clients would. Using your vehicle for rideshare apps such as Uber or Lyft, car sharing marketplaces like Turo, or food delivery services like DoorDash with a standard personal auto insurance policy requires additional coverage for the gaps in protection which Novo does not offer at this time. Vehicles being used for commercial purposes are ineligible for coverage at policy purchase, but if you decide to engage in this activity during your policy term, you should obtain coverage from another insurance company.

Restrictions may vary by state, but Novo does not offer coverage for commercial vehicles or vehicles used for business purposes such as ridesharing. Additionally, Novo does not offer coverage for motorcycles or exotic, classic, antique, recreational (RV), or offroad vehicles. If you are not the registered owner of the vehicle, have a high value or modified vehicle, salvage title, or recently filed a claim on the vehicle you are adding, there may also be restrictions in place depending on the situation. Your vehicle must be registered for street use and have a valid 17-character vehicle identification number (VIN). Please contact us to add your vehicle and for help with any questions you may have.

You can have up to 6 drivers and 4 vehicles listed in a single policy. Up to 2 drivers from your household may be excluded in the policy.

Novo’s standard policy term length is 6 months and will continue to automatically renew unless canceled by either Novo or the policyholder. We do not offer 1-year policy terms.

Novo's Flex plan typically offers the greatest potential for savings. Premiums for Flex are impacted by the way you actually drive, which is reflected in your Safety Score. The higher the score, the more premiums will decrease for a given month. Additionally, you can lower your monthly premiums by reducing coverage amounts from those which were selected when the policy was purchased or increasing your deductible. However, lowering coverages could put you at greater risk in the event of an accident and increasing the deductible could mean more out-of-pocket expenses.

There are many different factors that are used to calculate your policy premium, and they could vary by state. They may include age, years of driving experience, driving record (accidents and violations), geographic location, insurance-based financial responsibility score, gender, marital status, education, occupation, home ownership, insurance history (prior/continuous coverage), annual mileage driven, claims history, the vehicle(s) insured (year, make, model, trim, safety features, etc.), vehicle ownership status, and applicable discounts, among others. Coverage levels and deductibles can also be used to raise or lower premiums. With select Novo plans, the Safety Score is a key input for determining premium due.

If you get a new phone, you will not need to relink your vehicle within the Novo mobile app as long as the vehicle is paired with the phone via Bluetooth. If you add a new vehicle to your policy, you will be prompted to link it. The setup process will be similar to what you completed when you first purchased your policy.

You will have 4 weeks after your policy has become effective to link your vehicle(s). If you are unable to link your vehicle(s) within that timeframe, you may run the risk of losing any policy discounts that are associated with your insurance plan.

Novo does not require a paid connected services subscription for your vehicle. We are able to obtain your driving data either exclusively from your vehicle without an additional charge or from your vehicle in combination with your mobile phone. Standard mobile data rates may apply depending on your carrier and plan.

No additional action should be needed to connect most 2021+ Alfa Romeo, Chrysler, Dodge, Fiat, Jeep, and Ram vehicles. However, if you encounter any issues with your vehicle’s connectivity, you can contact Uconnect® by calling 1-877-855-8400. You can also visit www.driveuconnect.com for additional support.

All other years and makes will require you to perform the steps in this setup guide. When opening the Novo mobile app for the first time, it will also walk you through the setup process.

Alfa Romeo and Fiat are registered trademarks of FCA Group Marketing S.p.A. Chrysler, Dodge, Jeep, Ram, and Uconnect are registered trademarks of FCA US LLC.

Sometimes Novo may ask for photos of the vehicle during the underwriting review period (see "What is an underwriting review period?"). This helps us confirm there’s no existing damage when your policy starts. Having these photos can make the claims process faster if you ever file a comprehensive or collision claim. If we need photos from you, we’ll send clear instructions on how to submit them.

No, Novo does not offer non-owner policies for individuals who regularly drive but do not own a vehicle. Novo requires at least one vehicle on the policy.

No, Novo only offers personal auto insurance and policies are not designed for commercial vehicles or those engaging in business use, with some limited exceptions.

No, Novo does not offer coverage for trailers.

No, Novo does not offer coverage for motorcycles.

No, Novo’s personal auto policy is designed for private passenger vehicles — excluding exotic, classic, antique, recreational (RV), and offroad vehicles.

Your VIN is typically listed in several places on the vehicle including the dashboard near the windshield on the driver’s side and a plate or sticker attached to the driver's side door jamb. Documentation such as your insurance card/policy and title and registration should also include the VIN. If you are unable to locate your car's VIN, please contact the manufacturer for further assistance.

You must have one vehicle equipped with Bluetooth in order to enroll in either our Next or Flex plan which use driving data to help determine your rate or the Classic plan which offers a discount for sharing driving data. If there are additional vehicles that don't have Bluetooth, they are still eligible for coverage with us, but you will not have the option for premiums to change at renewal or from month to month based on a Safety Score because they will not have one available. If you have any questions about your vehicle’s eligibility, you can call us at 1-866-862-7757, chat with us at www.novo.us, or email support@novo.us. When you enter your VIN in our online quoting experience, we also perform a check to confirm that your car is compatible before allowing you to purchase coverage.

To enroll in our Next or Flex plans, which use driving data to help set your rate, or the Classic plan, which offers a discount for sharing driving data, you must have at least one vehicle equipped with Bluetooth (see "What insurance plans does Novo offer?”). You can still cover other vehicles without Bluetooth, but they won’t have a Safety Score available and therefore may not be eligible for discounts and savings associated with sharing driving data. All vehicles must have a gross vehicle weight rating (GVWR) under 12,000 lbs. When you enter your VIN during our online quote process, we’ll check if your car is compatible before you can purchase coverage. You can also call our customer support team if you have any questions.

Your insurance premium can change at different times: right away, each month, or at your policy renewal.

Immediate Changes: Your premium might change immediately if you update your policy. Some examples include adding or removing vehicles or drivers, changing your address, adjusting your coverage limits, or switching plans.

Monthly Changes (Flex plan only): If you have Novo’s Flex plan, your monthly premium can go up or down based on changes in your Safety Score (note: Classic and Next plans have fixed monthly premiums.)

Renewal Changes: Your premium may also change at renewal time. This depends on whether insurance rates in your state have gone up or down.

Yes, you are able to switch insurance plans at renewal if you feel that another one would be a better fit for you. Please call us at 1-866-862-7757, chat with us at www.novo.us (click the chat icon located at the bottom right corner), or email support@novo.us to change your plan. Changing plans may result in either an increase or decrease to your rate.

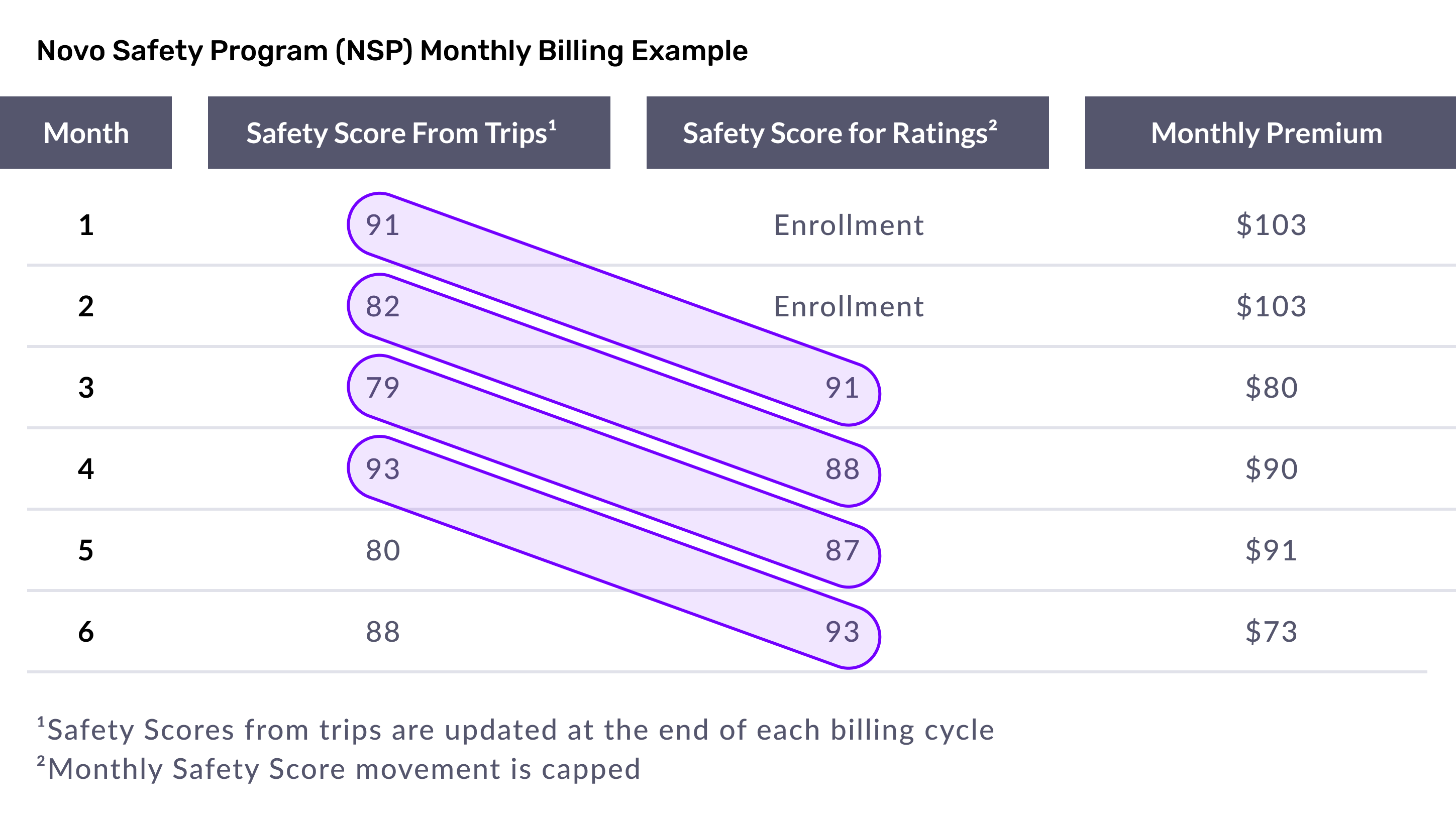

After you purchase a policy, the premium for the first 2 months will be locked in. If you have at least 30 days of historical driving data that we are able to access, your enrollment Safety Score for these 2 months will be based on that driving behavior. Otherwise, you will be provided with a default enrollment score with a discounted rate.

After 5 eligible trips, Novo will utilize your driving behavior to begin calculating your initial Safety Score as a policyholder on a scale of 1 to 100. This Safety Score will be used to determine your premiums after the first 2 months. The higher your score, the lower your premium will be. However, a lower score can result in increased premiums.

Month 3 will be the first month that is impacted by changes in your Safety Score based on driving behavior collected during month 1 of your policy. Then month 4’s premium is impacted by the Safety Score from month 2, and so on. There is always a 2-month gap between the Safety Score and the premium associated with that score so that drivers will have at least 30 days’ notice of any change in premium. Premiums may increase or decrease by as much as 60% or 38%, respectively, from one month to the next once you have established your first monthly Safety Score. However, most policyholders will see much smaller fluctuations in their month-to-month premiums.

Novo's Flex plan typically offers the highest potential savings vs. our other plans with premiums that change from month to month based on your actual driving behavior instead of remaining constant, only to go either up or down at renewal. We call this “real-time” insurance since the monthly premiums continually adapt to your driving style. This gives you more control over your expenses by allowing you to save more when you drive safer as measured by your Safety Score (see "What is Novo's Safety Score?").

The higher your Safety Score is each month, the lower your monthly rate will be in the corresponding bill, though your rate may also increase with risky driving (see "How does billing work for the Flex plan?"). Each monthly bill reflects your driving from the first to the last day of that billing cycle, which is based on your policy’s effective date. Driving data outside of that period counts toward the next bill. Rest assured, you’ll receive at least 30 days’ notice before any changes to your premium.

Novo’s Next plan is our intermediate option for drivers who prefer fixed monthly premiums but still want a personalized rate at renewal based on how they actually drive. The safer you drive—as measured by your Safety Score—the more you can save (see "What is Novo's Safety Score?"). While most customers earn a discount for safe driving, riskier driving may lead to a higher rate. Your cumulative Safety Score, measured up until about one month before your next policy term, will determine your renewal price and then reset for the next period. You'll always be notified at least 30 days in advance of any changes to your premium.

Novo's Classic plan is our more traditional insurance policy. It comes with an automatic 10% discount for sharing driving behavior so that we can provide insights and safety tips. However, any driving data that is shared will have no impact on your rate. Your Safety Score is for educational purposes only. Those with a high Safety Score may want to consider moving to our Next or Flex plans where the score is used to help determine the price you pay and unlock even more savings.

Usage-based insurance (UBI) is a type of auto insurance where your premium is based on how, how much, or how safely you drive—rather than solely on traditional factors like age, location, or driving history. UBI programs benefit both you and your insurer: you may qualify for lower rates and the insurer can price your policy more precisely using your driving data.

The specific factors used to measure safe driving can vary by insurer (see "What factors go into the Safety Score?" to learn how Novo evaluates driving). UBI is powered by telematics technology, which tracks your driving behavior and transmits the data to your insurer—usually through a mobile app or, in some cases, directly from your connected vehicle. UBI can be a great fit for drivers who want more control over what they pay for insurance—especially those who drive safely or want to improve their driving habits over time.

If you need assistance with the test drive program, you can contact our customer support team through the app or by visiting our website. For technical issues with the app, try restarting the application first. For questions about your driving data, quotes, or the transition to a full policy, our customer support is available to help. We also provide email communications at key points in the process to guide you through each step.

Unfortunately, Bluetooth connectivity is required for the test drive to function properly. If your phone doesn't support Bluetooth or you're experiencing persistent connectivity issues, you may not be able to participate in the program. We recommend ensuring your phone and vehicle both support Bluetooth connectivity before starting the program. If you continue to have technical difficulties, our support team can help troubleshoot or suggest alternative options.

Bluetooth should remain enabled on your phone for the app to properly track your trips. The app uses Bluetooth to detect when you're driving the registered vehicle and to collect trip data. Turning off Bluetooth will prevent the app from recording your trips, which could affect your ability to reach the minimum requirements for a Safety Score and quote.

If you encounter difficulties during setup, first ensure your phone's operating system is up to date and that you have a stable internet connection. Try restarting the app and your phone. Make sure you've enabled all requested permissions. If problems persist, you can contact our customer support team for personalized assistance with the setup process.

Driving data typically updates within a few minutes to a few hours after completing a trip. The app needs time to process and validate your trip data to ensure accuracy. If you notice delays longer than expected, check your Bluetooth connection and ensure the app has the necessary permissions. Your trip history and Safety Score are updated regularly, but not necessarily immediately after the a trip ends.

First, ensure that Bluetooth is enabled on your phone and that you're connected to your vehicle. Check that location services are enabled for the Novo app. Make sure you're driving the vehicle that's registered in your test drive account. If you're still having issues, try restarting the app or your phone. Remember that it may take a few minutes after completing a trip for it to appear in the app.

After becoming a policyholder, you can still receive referral rewards from previously referred users (within the limit) but cannot send new referrals. These rewards will be sent via email.

After becoming a Novo policyholder, you are still eligible to earn rewards from the referrals you made before becoming a policyholder. However, you will not be able to redeem gift cards from the app. Any remaining Amazon gift card balance will be sent via email within 24 hours after policy purchase.

Users can redeem their Amazon gift card reward directly in the mobile app if eligible. It will allow you to add the balance to your Amazon account. You may also request to have a redemption link emailed to your registered address.

If you do not already have the referral code, you will need to reach out to your friend or family member and obtain it to enter manually.

We highly recommend downloading the app via the unique link. This guarantees that we are able to correctly link the accounts and track reward eligibility. However, you may also enter the referral code manually during the account sign up process to claim the reward.

Novo's mobile app notifies both the referrer and referee when the reward is granted. Please make sure to allow push notifications in order to see when your reward is available.

Any number of people may register using a referral code, but only the first 10 who obtain a Safety Score will qualify for the reward.

A referrer can earn referral rewards for up to 10 successful referees who achieve a Safety Score. Beyond that, you can still refer to additional friends or family but will not be eligible for a reward.

Both the referrer and the referee receive a $10 Amazon gift card once they both have a Safety Score ready. This reward is only available if both are Arizona residents.

No. Referral, points, and rewards features are only available to users who are in Arizona. If a friend registers from outside Arizona, neither party will see or receive referral rewards.

Users can send referrals as soon as their Safety Score is ready in the app after their driving test.

Users registered for Novo's Test Drive can send a referral message using the app's sharing feature, which allows sending referrals through SMS, WhatsApp, Messenger, Facebook, Instagram, and other platforms. The app generates a unique referral link for easy sharing, so the new user does not need to enter a referral code manually.

Your test drive Safety Score directly impacts your insurance rate. The score you achieve during the trial period will be used to calculate your premium for the first 2 months of coverage with the Flex plan or 6 months with the Next plan (see "What insurance plans does Novo offer?"). After that, your ongoing driving performance will continue to influence your rate. This means the safe driving habits you develop during the test drive can lead to long-term savings.

Absolutely! Once you become a policyholder, your account will automatically transition to include all policyholder features. You'll get access to policy details, billing information, payment options, customer support features, and continued Safety Score tracking. The app will provide a brief orientation to help you understand these new features.

Your trip history from the most recent 30 days of your test drive experience will carry over to your new policyholder account. Your Safety Score from the test drive will be used for your enrollment rate. This ensures you get the benefit of the safe driving habits you demonstrated.

Your coverage will begin according to the effective date you select during the purchase process. You can choose to start coverage for the following day or another future date. Once you complete your purchase, you'll receive confirmation of your policy details and effective date.

While Novo's test drive is limited to 1 vehicle and 1 driver, you can add additional vehicles and drivers during the quoting process or even after policy purchase by contacting our customer support. The Safety Score from your test drive experience will apply to the vehicle you tested with. Additional vehicles and drivers will be rated according to our standard pricing methodology. This flexibility allows you to build the complete policy you need.

Yes, during the quoting process, you'll have the opportunity to review and modify your coverage options, add additional drivers or vehicles, and make other changes to customize your policy. Keep in mind that changes to your policy details may affect your final premium. The Safety Score you earned through the test drive will still be used to determine your premium.

When you're ready to purchase, tap the quote button in the app, which will take you to our web-based quoting process. This will open in your phone's browser where you can review your coverage options, make any necessary adjustments, and complete your purchase. Your driving data and Safety Score will automatically carry over to ensure you get the rate you earned through the program.

Your test drive quote is an estimate based on certain assumptions and defaults. While it's designed to be as accurate as possible, your final rate may vary when you complete the full quoting process, as we'll gather more detailed information about your specific coverage needs. However, your actual Safety Score from the test drive will be used in your final rate calculation, so the driving-based discount you earn is real.

Data from the test drive will only be used to provide a quote for either our Flex or Next plans (see "What insurance plans does Novo offer?”). However, you are still able to choose from any of our plans if you desire one different from the test drive offer.

You are unable to restart the test drive. However, you can keep driving to improve your Safety Score and your quote. Your quote will automatically update to reflect your latest score.

There are a few reasons why a quote might not be available. You may not have met all the minimum requirements (trips, miles, time period, and Safety Score), or our system may have been unable to verify your driving record through external sources. Additionally, if you're determined to be a high-risk driver based on past claims or violations, a quote may not be offered. The app will provide specific information about what's needed to qualify for a quote.

Your quote is good for a limited time. If you wait to purchase, your rate may change as new driving data is collected over time. For the most accurate and up-to-date pricing, we recommend purchasing your policy soon after receiving your quote.

To receive your quote, we'll need basic personal information including your full name, date of birth, and home address. We'll also need your vehicle details (year, make, model). Additionally, you'll also need to complete the minimum driving requirements and have a Safety Score of at least 85. All of this information helps us calculate the most accurate quote possible for your specific situation.

Arizona residents can see their personalized quote after meeting the driving requirements (5 trips and 200 miles, or 5 trips and 50 miles after 2 weeks) and providing some basic personal information. There's also a minimum waiting period to ensure we have enough data for an accurate quote. Most customers will see their Safety Score within 14 days of regular driving. The app will notify you when your quote is ready.

Your Safety Score will be revealed after you complete 5 trips and drive 200 miles. If you haven't reached these minimums after 2 weeks, we'll show your score once you've completed 5 trips and 50 miles. The app will keep you updated on your progress toward these requirements with a trip and mileage countdown.

You can stop at any time by logging out of the app or deleting your account. There are no penalties or fees for discontinuing the trial. If you log out, trip data collection will stop immediately, but you can still log back in to view your past scores and trips. You're under no obligation to purchase insurance, even after completing the full test drive experience.

No, it is completely free to use. There are no charges for downloading the app, participating in the program, or receiving your personalized quote. You only pay if you decide to purchase a policy, and even then, you'll benefit from any discounts you've earned through your safe driving during the trial period.

Getting started is simple. First, download the Novo app from your device's app store (see "How do I get the Novo app?"). When you open the app, choose to sign up as a new user and register with your email address. You'll receive a one-time password via email to verify your account. After signing up, you'll add your vehicle information and set up Bluetooth connectivity (see "How do I connect my vehicle?"). Once everything is configured, just drive normally and let the app track your trips.

Your vehicle must be equipped with Bluetooth and not used for commercial purposes in order to take a test drive. When you add your car in the app, we'll verify its eligibility based on the year, make, model. If your vehicle doesn't support Bluetooth or isn't compatible with our system, the app will let you know during the setup process. Vehicle eligibility requirements are designed to ensure we can accurately collect your driving data.

Currently, the test drive program is available for anyone to download and get a Safety Score, but only Arizona residents are currently eligible to receive an insurance quote and purchase a policy. You'll need a Bluetooth-compatible vehicle and a smartphone to participate. The program is designed for drivers who have some time to make a purchase decision (typically 1-4 weeks) and want to see real savings based on their driving habits.

Novo's test drive is a trial program that lets you experience our safety-based auto insurance pricing before committing to a policy. You'll download our app, connect your vehicle via Bluetooth, drive normally for a period of time, and receive a quote based on your actual driving habits — with savings up to 40%. This gives you the opportunity to see your personalized price with Novo before you switch.

While our goal is always to pay claims as quickly as possible, the amount of time it can take to close a claim can vary. There are times during the claims process when we need to wait on third parties for external reviews and appraisals before we can approve and ultimately close a claim. Certain claims such as those involving bodily injury liability may also take longer to settle than a simple fender bender. Additionally, if the claimant is missing information and unable to provide all necessary documentation in a timely manner, this could also lead to delays in the claims process.

If your vehicle is a total loss, you should begin by removing all personal items from the vehicle along with the license plates and all documentation that would typically be stored in the glove box. You should make sure to obtain your vehicle title and if your lender still has it, provide authorization to release it to us along with the loan payoff information. If you’ve taken out a loan or leased your vehicle, you should let your lender or leasing company know that the vehicle was totaled and that your insurance company will be in contact with them.

There are occurrences where a total loss payment may be less than the total amount left on your loan or lease. You should consult with your lender in these situations to understand who is responsible for the difference. In most agreements, you would be responsible for paying the gap between the unpaid amount due on your loan or lease and the actual cash value of your totaled vehicle. If you purchased loan-lease payoff coverage, we would pay for the balance up to 25% of the actual cash value of the vehicle. If you did not purchase this coverage, we would only pay the actual cash value of the vehicle up to the policy limits, minus the applicable deductible listed in your policy.

In the event of a total loss, payment may go to you, the lender, or both. If you do not fully own the vehicle and have an outstanding loan, we will send the payment directly to the lender first. If there's a remaining balance after we pay the lender, then we'll send it to you. If the claim payment is not enough to cover your loan, you'll likely be responsible for paying off the balance to your lender. With loan-lease payoff coverage, we would pay for the difference up to 25% of the actual cash value of the vehicle. If you fully own the vehicle, the entire payment will be sent to you. We may request proof of ownership for total loss vehicles before we issue payment. For leased vehicles, we’ll issue payment directly to the leasing company.

If your vehicle is totaled and you would like it removed from your policy, you must notify us since we do not have the ability to make changes to your policy without consent. If you decide to retain a totaled vehicle and want to keep it insured, you must submit proof that it was repaired and evaluated to be roadworthy, or it would be subject to removal under state requirements. In addition, if the vehicle is the only one on the policy, you may want to keep the policy in place until you purchase a replacement vehicle in order to avoid a lapse in coverage. Electing to cancel the policy until a new vehicle is purchased could result in a lapse in coverage which can increase your rates, result in state fees, and impact your ability to secure a policy with some insurance companies. In this situation, it is recommended that you reach out to a customer service rep to review your coverages and reduce your rates until you have a replacement vehicle to add to the policy.

In most cases, you are able to keep your vehicle if you so choose. However, if you decide on that option, we will need to deduct the salvage value from the settlement amount. The salvage value is the amount that we would estimate we would receive by selling it to a salvage yard, auctioning it off to the highest bidder, or selling it to third-party companies which specialize in repairing and reselling totaled vehicles. If you keep the vehicle, some states may require you to update the title to indicate a total loss and go through a state inspection process before it is deemed roadworthy after repairs and able to be reregistered.

While the definition can vary by state, a vehicle is usually considered a total loss when the cost to repair and return it to its pre-loss condition is greater than the value of the vehicle. In some states, the repair costs may need to only exceed a certain percentage of the vehicle’s value. For total losses, repairs are not economical or practical to safely restore to pre-accident condition. The claim payment would equal the actual cash value (the market value) of the vehicle minus your deductible.

We may include new OEM parts in your estimate for repairs for newer vehicles. For older vehicles, we usually include quality replacement parts from other manufacturers or used parts, depending on availability of the part. Some parts may only be available from the OEM, and there are cases where those parts have been discontinued and no longer available to order. If you choose OEM parts when quality aftermarket options are available, you'll be responsible for any cost differences in most states.

A supplement is an additional request from the repair facility for funds beyond the original estimate for further damage which was found. This ensures that your vehicle is repaired to its pre-accident condition and that nothing was overlooked.

Finding additional damage during the repair process is relatively common. If there is additional loss-related damage beyond what was identified in the initial inspection, your adjuster will re-inspect your vehicle and work with you and the repair shop to update the estimate. The repair facility will submit a supplemental estimate which will outline any newly identified damage, additional repairs required, and the associated costs. After approval, they will continue with the repair until completion. In some cases where the newly found damage is significant, the vehicle could be declared a total loss as a result of the supplement.

Every claim is different depending on the extent of the damage, types of injuries, and speed of the selected repair facility. We work to get you and your vehicle back on the road as quickly as possible, but there are many factors that can potentially impact how long that might take. It could be as short as a few weeks or take several months or longer for a complex investigation. Making sure that you provide all requested documentation in a timely manner will help us to do so more efficiently.

Yes, you will be required to pay the difference in costs between the standard rental vehicle and any voluntary upgrade. However, you usually would not be charged for upgrades due to lack of available inventory from the rental facility. Company policies for this scenario may differ between rental car providers.

You are able to keep the rental vehicle for the period of time reasonably required to repair, replace, or reimburse for the value of the vehicle or until your overall rental limit of 30 days is exhausted, whichever comes first. This also applies to total losses such as your vehicle being stolen and not recovered.